Leaning on the Megabanks Can Pay Off, if You've Got a Little Muscle and a Lot of Patience

Banks had paid $21 billion through this past summer to repurchase souring home loans from Fannie Mae and Freddie Mac, the taxpayer-backed mortgage companies, under contracts that oblige lenders or loan servicers to buy back loans that aren't up to snuff.

That covers about 13% of the mortgage companies' credit losses since their government takeover, according to a report released this month by the Financial Crisis Inquiry Commission.

Yet it's just a sliver of the $529 billion of profits U.S. banks booked during the heyday of the housing bubble, between 2003 and 2006 -- and it may be just a small fraction of the sums they will fork over in looming mortgage battles with insurers and private investors.

Banks That Have Repurchased the Most Loans from Fannie Mae -

Bank of America - $5.8 Billion

JP Morgan Chase - $3.6 Billion

Wells Fargo - $2.9 Billion

GMAC/Ally - $1.2 Billion

Suntrust - $1.1 Billion

Citigroup - $1.1 Billion

Estimates of bank exposure to so-called private label mortgage put-backs run into the tens of billions. Settling remaining claims by Fannie and Freddie, by contrast, may not cost much more than a few billion - which makes it that much more exasperating to see the banks playing their foot-dragging games.

The bank that has gotten the most bad mortgages bounced back to it by Fannie and Freddie is, no surprise, Bank of America, the North Carolina-based owner of the notorious Countrywide subprime mill. Over the past four years, it got $6.9 billion in repurchase requests from Fannie alone – as much as its next four competitors combined.

Data released by the FCIC show the bank paid Fannie and Freddie almost $6 billion over the past four years to settle mortgage repurchase requests – and that was before the settlement this month under which it forked over an added $2.8 billion.

Yet despite that show of comity, the banks aren't going quietly. For every three bad loans repurchased as of September, there were two more requests from Fannie and Freddie that the banks hadn't honored.

That number has come down some since Bank of America and Ally, formerly known as GMAC, agreed to settlements with Fannie and Freddie. Even so, some $10 billion of repurchase requests remain open – and there is some evidence the banks have been dragging their feet in paying up.

As of September, about a third of the outstanding repurchase requests issued by Fannie and Freddie had been outstanding for at least four months, the companies said in their latest quarterly filings with regulators. Banks, "including many of our larger seller/servicers, have not fully performed their repurchase obligations in a timely manner," Freddie noted in its filing.

The firm went on to say the banks' tardiness had caused it to "begun to require certain of our larger seller/servicers to commit to plans for completing repurchases, with financial consequences or with stated remedies for non-compliance, as part of the annual renewals of our contracts with them."

The struggles of Fannie and Freddie to collect on their repurchase demands are remarkable because rules are on the government-sponsored entities' side. The contracts they sign with mortgage originators and servicers give Fannie and Freddie the clear right to force bankers to buy back loans that fail to meet the companies' guidelines.

By contrast, the rules in private label disputes – ones pitting the banks with investors such as pension funds that bought mortgage-backed bonds without Fannie and Freddie's involvement – are much murkier, a situation the banks expect to use to their advantage.

Even so, analysts at Deutsche Bank, for instance, expect Bank of America to shell out $15 billion or so to settle private label mortgage disputes in coming years -- well above the $9 billion analysts expect it to pay to settle its Fannie-Freddie liabilities. That's because the underwriting on the private label bonds tends to have been so much worse, which has translated into many more suspicious-looking early defaults to make good on.

In contrast, the numbers presented in the FCIC report make most of the big banks' exposure to Fannie Mae mortgage repurchases look downright manageable. Were they to settle on the same terms as BofA, for instance, Wells Fargo would pay Fannie $321 million, Citi $247 million and JPMorgan Chase $193 million. Unlike Fannie, Freddie Mac didn't disclose outstanding repurchase requests by bank in its FCIC submissions.

But now that the worst actor, Countrywide, has cleared up many of its disputes with the GSEs, the stakes are apparently so low that no one is in a hurry to settle.

"It's kind of the moot point, but if [Fannie and Freddie] wanted to settle it all at once, it'd be fine with us," JP Morgan Chase chief Jamie Dimon said.

Monday, January 31, 2011

Friday, January 28, 2011

Reuters Poll: Housing Bottom Seen in Mid - 2011

U.S. house prices are likely to continue to slide before bottoming out sometime in the middle of this year but will rise just over two percent in 2011 as a whole, according to economists polled by Reuters.

Asked when they see a bottom for U.S. house prices, 14 of 26 economists said they would trough in either the second or third quarter of 2011. Three saw the bottom coming as early as this quarter, while one did not see a bottom until the first three months of 2014.

"A pullback in prices following the expiration of the homebuyers tax credit was not a surprise. Ultimately, a recovery in the housing sector will depend critically on the job market, which should improve over time," said Scott Brown at Raymond James.

The Standard & Poor's/Case-Shiller composite index of 20 metropolitan areas, which has struggled since home-buyer tax credits expired earlier this year, declined 0.5 percent in November from October on a seasonally adjusted basis, the fifth straight monthly decline in home prices.

Asked how much further prices would fall before stabilizing, the median response of 24 economists who answered was another 3.3 percent drop from current levels. Two economists saw a further decline as sharp as 10 percent.

But medians showed prices, which economists say will have lost a third of their value from peak to trough, would rise 2.1 percent this year, up from the 1.0 percent prediction in a poll taken in November.

Economists saw house prices as fairly valued now. Asked to rate current prices on a scale of 1-10, with 10 being overvalued and 1 being undervalued, 27 of 32 respondents answered with a 4, 5 or 6. Just one responded with a 7 and one responded with a 2.

The average home sales price in the United States was $169,800 in the fourth quarter of 2010, according to the National Association of Realtors.

Sales of U.S. new homes raced to their highest level in eight months in December, but gains were driven by a surge in the West. Even with last month's gain, new-home sales are down 75 percent from their peak of 1.283 million-unit pace in 2005.

"Housing is showing a ray of hope, but is still far from healed," said Diane Swonk of Mesirow Financial. "The level of activity in the market, in particular new home sales, will take much longer to recover to reasonable levels."

The poll was conducted over the past week and included a total of 33 economists.

Asked when they see a bottom for U.S. house prices, 14 of 26 economists said they would trough in either the second or third quarter of 2011. Three saw the bottom coming as early as this quarter, while one did not see a bottom until the first three months of 2014.

"A pullback in prices following the expiration of the homebuyers tax credit was not a surprise. Ultimately, a recovery in the housing sector will depend critically on the job market, which should improve over time," said Scott Brown at Raymond James.

The Standard & Poor's/Case-Shiller composite index of 20 metropolitan areas, which has struggled since home-buyer tax credits expired earlier this year, declined 0.5 percent in November from October on a seasonally adjusted basis, the fifth straight monthly decline in home prices.

Asked how much further prices would fall before stabilizing, the median response of 24 economists who answered was another 3.3 percent drop from current levels. Two economists saw a further decline as sharp as 10 percent.

But medians showed prices, which economists say will have lost a third of their value from peak to trough, would rise 2.1 percent this year, up from the 1.0 percent prediction in a poll taken in November.

Economists saw house prices as fairly valued now. Asked to rate current prices on a scale of 1-10, with 10 being overvalued and 1 being undervalued, 27 of 32 respondents answered with a 4, 5 or 6. Just one responded with a 7 and one responded with a 2.

The average home sales price in the United States was $169,800 in the fourth quarter of 2010, according to the National Association of Realtors.

Sales of U.S. new homes raced to their highest level in eight months in December, but gains were driven by a surge in the West. Even with last month's gain, new-home sales are down 75 percent from their peak of 1.283 million-unit pace in 2005.

"Housing is showing a ray of hope, but is still far from healed," said Diane Swonk of Mesirow Financial. "The level of activity in the market, in particular new home sales, will take much longer to recover to reasonable levels."

The poll was conducted over the past week and included a total of 33 economists.

Adjustable-rate Mortages May be Making a Comeback

5/1 Hybrid is the Most Popular ARM Today

After years of virtual exile from the home loan arena, is the adjustable-rate mortgage staging a quiet comeback? Could an ARM be on your shopping list the next time you need to buy a house or refinance?You might be surprised.

A new survey of 112 lenders by mortgage giant Freddie Mac found that ARMs are starting to attract applicants again. Adjustables accounted for just 3 percent of new home loans in early 2009, but are projected to be the final choice for nearly one out of 10 borrowers in 2011. In the jumbo and super-jumbo segments, the share will be even larger, according to Freddie Mac chief economist Frank Nothaft.

How could this be, with fixed 30-year rates at half-century lows, hovering just under 5 percent? Isn't it axiomatic that it's always smarter to lock in a low fixed rate for as long as possible rather than to gamble on a loan whose rate might bounce around in the years ahead?

That logic still holds up for most people, but not for everybody. Here's why. The boom-era models of the ARM have pretty much disappeared -- there are no more of the two-year adjustables that hooked record numbers of consumers in 2003 and 2004 with teaser rates that needed to be refinanced with heavy fees within 24 months. No more "pick-a-pay" ARMs that were mass-marketed with loosey-goosey underwriting and negative amortization.

The most popular ARM in the market today, according to the Freddie Mac survey, is the "5-1" hybrid. Its rate is fixed for the first five years of the loan, then adjusts annually for as much as the next 25 years, with protective rate caps to cushion payment shocks if rates suddenly spike. There are also "7-1" and "3-1" hybrids. The antique one-year ARM still is available but doesn't get a lot of takers.

The real key to the growing popularity of hybrid ARMs is in their pricing.

Rates are significantly lower than fixed 30-year alternatives, with no teasers or negative amortization involved. In some cases, they also come with other attractive terms, such as more flexible underwriting standards.

According to data supplied by Dan Green, a loan officer with Waterstone Mortgage Corp. in Cincinnati and author of TheMortgageReports.com blog, the rate spread between 5-1 hybrid ARMs and 30-year fixed-rate loans has now widened to around 1.625 percentage points.

To illustrate, say you're interested in a $250,000 conventional loan to buy a house. You've got a 740 FICO credit score and want to close in 45 days. You could opt for a 30-year fixed loan at 4.75 percent, requiring a monthly principal and interest payment of $1,304. Alternatively, you could opt for a 5-1 ARM fixed at 3.125 percent, costing $1,071 in principal and interest per month - a $233 saving.

But now check out the niche where hybrid ARMs really shine: Jumbo and super-jumbo mortgages.

Generally jumbos range from $417,000 to $729,750, depending on home prices in your local market. Super jumbos can go into the millions.

Say you need a $450,000 mortgage with a 45-day closing and you have a 740 FICO.

According to Green, you should be able to get a 30-year fixed rate jumbo today for around 5.625 percent. Monthly principal and interest on a fixed rate jumbo would total $2,590 a month. Compare that with a $450,000 hybrid 5-1 ARM: 3.5 percent for the initial five years, requiring $2,020 a month in principal and interest. That's a rate spread of 2.125 points -- "the best we've seen in years," said Green in an interview. "It's very aggressively priced" by banks who want to originate them to hold in their own portfolios.

The savings go even higher in the super-jumbo space -- a $1 million 5-1 ARM goes for 3.5 percent and saves a borrower $1,266 a month compared with a competing $1 million fixed rate 30-year loan at 5.6 percent.

Cathy Warshawsky, president and senior loan officer of Bay Area Loan Inc. in San Jose, Calif., cites another advantage for some jumbo borrowers -- special enhancements in payment terms. For example, a client of Warshawsky's needed a $950,000 mortgage at the lowest rate and monthly payment.

She signed him up for a 5-1 hybrid at 5.75 percent, interest-only.

None of this is to suggest, of course, that hybrid adjustables make financial sense for everybody.

They don't.

But if you fit one of the niches -- you need a jumbo, you know you're likely to be transferred or you expect to sell the house within the coming five to seven years -- they merit a serious look.

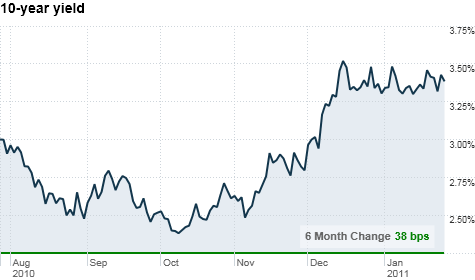

What Bonds are Saying About Inflation

The 10 Year Treasury and certain Mortgage-Backed Securities can have a daily effect on mortgage rates.

Like a dripping faucet filling up a sink, yields on U.S. Treasuries have been slowly rising for several months now -- raising concerns that inflation may be on the horizon. Higher Treasury yields are a direct result of the Federal Reserve's near-0%interest rates and its massive quantitative easing strategy, combined with a slowly improving but sluggish economy.

On many fronts, inflation is already here. Oil prices are up 17% from a year ago, and wheat, cattle and coffee prices have all posted doubled-digit increases, deepening worries about skyrocketing food prices.

As fuel prices and food prices keep rising, no one is using the "s" word yet, but there are some whispers of the dreaded stagflation - a condition of low economic growth in an inflationary environment.

We're not necessarily bracing for a return to the 1970s era of Jimmy Carter sweaters and long gas lines. But with the an unemployment rate of 9.4% and oil at $87 a barrel - it's not the prettiest picture. On top of that, the first look at fourth-quarter GDP showed growth but fell short of forecasts. "Frankly we need a little inflation right now, it would show the economy is expanding," Feinman said.

Bond rates are still low. Still, fears about inflation and stagflation shouldn't be overblown. Consumers are starting to spend again. Holiday sales were strong and consumer spending in the fourth quarter expanded at its fastest rate in five years, according to the Commerce Department.

So that brings us back to bond prices. The U.S. Treasury yield curve -- a graph of the interest rates on government bonds with different maturities -- has steepened noticeably, which typically signals economic expansion and the possibility of inflation.

Just six months ago, the curve was much flatter, with investors still talking about the possibly of deflation or even a double-dip recession. The yield on the benchmark 10-year note is currently hovering around 3.4%, compared with the 2.6% level it was at back in September.

"On balance, the general economic picture has been better and the growth prospects have been getting better," said Josh Feinman, an economist at Deutsche Bank. "Bond yields are rising because we are no longer concerned at all about deflation or even a double-dip."

But for bond investors who buy investments to hold for months or even years, it's not what inflation is now that matters, it's what it it's going to be down the road. "The bond market is pricing things in that may happen six months, 12 months, two years down the road, long before this will happen" said Ken Naehu, portfolio manager with Bel-Air Investment Advisors, who manages about $6 billion in assets for mostly high net-worth clients.

If the recovery gains momentum and the threat of inflation becomes a reality, some experts are concerned the Fed may be caught with its pants down, figuratively speaking. Most economists expect the central bank will keep a 0% interest rate policy at least until the second half of this year or maybe into 2012 by some estimates.

"The longer they keep rates where they are, the faster they are going to have to raise them," said Adolfo Laurenti, an economist with Mesirow Financial in Chicago. "That makes the market a bit concerned."

Thursday, January 27, 2011

8 Reasons to Invest in Your Home

Not long ago, you could have your big remodeling project and get your money back too. Owners recouped an average of 87% of home improvement costs at resale in 2005, according to Remodeling magazine.

But by 2010 the magazine had pegged the typical payback at just 60%. Hardly the right time to tackle the new kitchen or master bathroom you've been dreaming of, right?

Not so fast, says Kermit Baker, senior research fellow at Harvard University's Joint Center for Housing Studies. "In many cases, these projects make more sense now than they did at the height of the market," he said.

Assuming you like what you can't change about your home -- the neighborhood, the school district, the proximity to things that matter to you -- and you're planning on staying for five or more years, improving your home is a smart move. Here's why.

1. Funding is cheap

The current economic climate sweetens the pot for people on solid financial footing.

Should I spend $60,000 to renovate my house?

"The Fed doesn't want you to save -- it wants you to put your dollars into circulation," said Keith Gumbinger, mortgage market analyst at HSH.com.

Today's historically low interest rates mean that most home-equity lines of credit are charging their floor rates (your HELOC's probably is around 3% if you've held it for a couple of years, 4% or 5% if the loan is more recent).

And with the typical bank account and money fund paying far less than 1%, drawing down your savings barely costs you anything in lost income -- just don't jeopardize your safety cushion.

2. Eager contractors are discounting

Although the construction industry rebounded somewhat last year, business is still slow. Remember when getting a contractor to call you back was a challenge?

Now the best pros in town will happily bid on your job -- and they'll probably offer you prices that are 10% to 20% below what you would have paid when real estate was going gangbusters, according to Bernard Markstein, senior economist for the National Association of Home Builders.

3. Materials have come down

The cost of building supplies has tumbled too. Plywood is down 23% since its peak in the mid-2000s. Drywall is off 29%, framing lumber 35%.

Not all raw materials prices have fallen that much: Asphalt roofing, which is made from a petroleum byproduct, is down only 7% over the past two years. Insulation -- which has been in high demand because of energy rebates and high fuel prices -- is down a mere 2% since 2006. Still, on the whole, construction supplies are bargains right now.

4. You'll cut your energy costs

You don't have to hire a green builder to see energy savings from a renovation. In a prewar house in the high-energy-cost Northeast, for example, a standard kitchen remodel could cut your utility expenses by $400 a year thanks to new insulation, windows, and appliances.

Even years of such savings will never come close to covering the project's price tag, but think of your lower electric and heating bills as an annual dividend.

5. Fixing up costs less than trading up

With the median home price down 22% since 2006, you might think this is an opportune time to trade up for the new master bathroom or other modern feature you want. After all, why not buy somebody else's remodeling headache at a discount.

0:00 /2:11Home improvement goes green

But you can't assume that you'll easily sell your house in this tough market and then find a new place that has the exact features you want (and not a bunch of stuff you don't want). And moving remains far costlier than improving, said John Ranco, past president of the Greater Boston Association of Realtors.

For starters, commissions and fees to sell a $400,000 home could run $25,000.

"You can get a lot of remodeling done for that kind of money," said Ranco. "And that doesn't even include the higher price you're paying for the new house, the moving costs, or the inevitable painting and window treatments the new place will need."

6. You can keep that sub-5% mortgage

As long as you're not underwater and haven't wrecked your credit, you've been able to take advantage of recent rock-bottom interest rates to lock in a fixed-rate mortgage below 5%.

Move several years from now, and you'll have to give up that loan, probably for something in the sixes or sevens, said Harvard's Baker. That's not bad, but it could mean hundreds a month in added interest costs.

"If you can remodel your way into staying put long term, you can hold on to that once-in-a-lifetime rate," says Baker.

7. Smart projects still add value

In the post-boom era, the rule of thumb for gauging the potential payback from a home improvement is simple: If you're bringing your house in line with similar homes in the area, you'll most likely earn back the lion's share of the cost when you sell. If you're surpassing the neighborhood, you probably won't.

"Remodeling a 10-year-old kitchen because you don't like its style doesn't pay anymore," says Thomas Collimore, director of investor education for the CFA Institute. "But replacing a 1960s kitchen is a different story."

At least for the foreseeable future, buyers will either lowball their bids or pass on your house entirely unless you've already tackled this kind of deferred renovation.

8. You get to enjoy the results

When it comes time to sell your place, chances are you'll probably wind up having to do the sorely needed renovations you didn't take care of earlier. Not only does that add a huge amount of stress to the process of putting a house on the market, but you still end up spending the money (quite possibly when contractor, materials, and borrowing costs are higher).

Why not get the benefits of a new furnace or an updated powder room for you and your family instead of buying them for the house's next owners? And why not do the projects soon so you get as much time as possible to enjoy the results?

Unlike vacations, luxury cars, or other discretionary expenditures, your remodeling project might recoup a significant chunk of its cost someday.

Even so, home improvements aren't purely investment decisions -- you shouldn't redo a kitchen or bathroom in the hopes of making a profit. But if you want to upgrade the quality of your home life and you can afford the cost, it's money well spent. To top of page

But by 2010 the magazine had pegged the typical payback at just 60%. Hardly the right time to tackle the new kitchen or master bathroom you've been dreaming of, right?

Not so fast, says Kermit Baker, senior research fellow at Harvard University's Joint Center for Housing Studies. "In many cases, these projects make more sense now than they did at the height of the market," he said.

Assuming you like what you can't change about your home -- the neighborhood, the school district, the proximity to things that matter to you -- and you're planning on staying for five or more years, improving your home is a smart move. Here's why.

1. Funding is cheap

The current economic climate sweetens the pot for people on solid financial footing.

Should I spend $60,000 to renovate my house?

"The Fed doesn't want you to save -- it wants you to put your dollars into circulation," said Keith Gumbinger, mortgage market analyst at HSH.com.

Today's historically low interest rates mean that most home-equity lines of credit are charging their floor rates (your HELOC's probably is around 3% if you've held it for a couple of years, 4% or 5% if the loan is more recent).

And with the typical bank account and money fund paying far less than 1%, drawing down your savings barely costs you anything in lost income -- just don't jeopardize your safety cushion.

2. Eager contractors are discounting

Although the construction industry rebounded somewhat last year, business is still slow. Remember when getting a contractor to call you back was a challenge?

Now the best pros in town will happily bid on your job -- and they'll probably offer you prices that are 10% to 20% below what you would have paid when real estate was going gangbusters, according to Bernard Markstein, senior economist for the National Association of Home Builders.

3. Materials have come down

The cost of building supplies has tumbled too. Plywood is down 23% since its peak in the mid-2000s. Drywall is off 29%, framing lumber 35%.

Not all raw materials prices have fallen that much: Asphalt roofing, which is made from a petroleum byproduct, is down only 7% over the past two years. Insulation -- which has been in high demand because of energy rebates and high fuel prices -- is down a mere 2% since 2006. Still, on the whole, construction supplies are bargains right now.

4. You'll cut your energy costs

You don't have to hire a green builder to see energy savings from a renovation. In a prewar house in the high-energy-cost Northeast, for example, a standard kitchen remodel could cut your utility expenses by $400 a year thanks to new insulation, windows, and appliances.

Even years of such savings will never come close to covering the project's price tag, but think of your lower electric and heating bills as an annual dividend.

5. Fixing up costs less than trading up

With the median home price down 22% since 2006, you might think this is an opportune time to trade up for the new master bathroom or other modern feature you want. After all, why not buy somebody else's remodeling headache at a discount.

0:00 /2:11Home improvement goes green

But you can't assume that you'll easily sell your house in this tough market and then find a new place that has the exact features you want (and not a bunch of stuff you don't want). And moving remains far costlier than improving, said John Ranco, past president of the Greater Boston Association of Realtors.

For starters, commissions and fees to sell a $400,000 home could run $25,000.

"You can get a lot of remodeling done for that kind of money," said Ranco. "And that doesn't even include the higher price you're paying for the new house, the moving costs, or the inevitable painting and window treatments the new place will need."

6. You can keep that sub-5% mortgage

As long as you're not underwater and haven't wrecked your credit, you've been able to take advantage of recent rock-bottom interest rates to lock in a fixed-rate mortgage below 5%.

Move several years from now, and you'll have to give up that loan, probably for something in the sixes or sevens, said Harvard's Baker. That's not bad, but it could mean hundreds a month in added interest costs.

"If you can remodel your way into staying put long term, you can hold on to that once-in-a-lifetime rate," says Baker.

7. Smart projects still add value

In the post-boom era, the rule of thumb for gauging the potential payback from a home improvement is simple: If you're bringing your house in line with similar homes in the area, you'll most likely earn back the lion's share of the cost when you sell. If you're surpassing the neighborhood, you probably won't.

"Remodeling a 10-year-old kitchen because you don't like its style doesn't pay anymore," says Thomas Collimore, director of investor education for the CFA Institute. "But replacing a 1960s kitchen is a different story."

At least for the foreseeable future, buyers will either lowball their bids or pass on your house entirely unless you've already tackled this kind of deferred renovation.

8. You get to enjoy the results

When it comes time to sell your place, chances are you'll probably wind up having to do the sorely needed renovations you didn't take care of earlier. Not only does that add a huge amount of stress to the process of putting a house on the market, but you still end up spending the money (quite possibly when contractor, materials, and borrowing costs are higher).

Why not get the benefits of a new furnace or an updated powder room for you and your family instead of buying them for the house's next owners? And why not do the projects soon so you get as much time as possible to enjoy the results?

Unlike vacations, luxury cars, or other discretionary expenditures, your remodeling project might recoup a significant chunk of its cost someday.

Even so, home improvements aren't purely investment decisions -- you shouldn't redo a kitchen or bathroom in the hopes of making a profit. But if you want to upgrade the quality of your home life and you can afford the cost, it's money well spent. To top of page

Wednesday, January 26, 2011

New Home Sales Jump to 8-Month High

New home sales climbed 17.5% in December to the highest level in eight months, the government reported Wednesday.

Sales of newly built single-family homes rose to an annual rate of 329,000 units last month, from a revised 280,000 units the month before, the Commerce Department said. That was the highest level since April. But compared with 2009, sales are down 7.6%.

The monthly sales figure was higher than the annual rate of 300,000 analysts surveyed by Briefing.com had expected.

"Though it's better than expected, we're still not getting a serious rebound," said Doug Roberts, chief investment strategist for Channel Capital Research. "This is a U-shaped situation, where we can have monthly blips when it's positive, but we're going to be bouncing along the bottom for a while."

Sales may have been boosted by homebuilders clearing out inventories at discounted rates at the end of the year, he said.

8 reasons to invest in your home

"People like to get their books in order at the end of the year," Roberts said. "It's akin to retailers clearing out inventory -- it's not getting any better so they don't want to hold onto it."

To clear out this inventory, Roberts said homebuilders have been offering special deals, like offering to throw in a granite counter-top instead of a standard one.

The median sales price of new homes was $241,500, up from $215,500 the month before, the government reported. At the end of December, 190,000 new homes were for sale, equal to a 6.9-month supply at the current pace.

While inventory was down from the 8-month supply available at the end of November, Roberts said homebuilders worry that foreclosures entering the market could cause supplies to swell.

"Foreclosures can act as competition to new home sales, so if they really start to resume that could have a negative impact," he said. "When banks take possession, they have to pay insurance and are responsible for taxes -- so everyone is saying they hope the situation improves so they don't have to write down more foreclosures, but they aren't disappearing yet."

Roberts said it will likely take a couple of years -- and maybe even five or six -- for homebuilders to make a significant dent in inventories and for home sales to really begin recovering.

"Housing tends to be a long cycle, where it does really well for a long time and then you go down and stabilize for a long time as well," said Roberts. "For now sales will bounce up and down, but long term I don't think anyone is talking about a shortage of homes out there."

Sales of newly built single-family homes rose to an annual rate of 329,000 units last month, from a revised 280,000 units the month before, the Commerce Department said. That was the highest level since April. But compared with 2009, sales are down 7.6%.

The monthly sales figure was higher than the annual rate of 300,000 analysts surveyed by Briefing.com had expected.

"Though it's better than expected, we're still not getting a serious rebound," said Doug Roberts, chief investment strategist for Channel Capital Research. "This is a U-shaped situation, where we can have monthly blips when it's positive, but we're going to be bouncing along the bottom for a while."

Sales may have been boosted by homebuilders clearing out inventories at discounted rates at the end of the year, he said.

8 reasons to invest in your home

"People like to get their books in order at the end of the year," Roberts said. "It's akin to retailers clearing out inventory -- it's not getting any better so they don't want to hold onto it."

To clear out this inventory, Roberts said homebuilders have been offering special deals, like offering to throw in a granite counter-top instead of a standard one.

The median sales price of new homes was $241,500, up from $215,500 the month before, the government reported. At the end of December, 190,000 new homes were for sale, equal to a 6.9-month supply at the current pace.

While inventory was down from the 8-month supply available at the end of November, Roberts said homebuilders worry that foreclosures entering the market could cause supplies to swell.

"Foreclosures can act as competition to new home sales, so if they really start to resume that could have a negative impact," he said. "When banks take possession, they have to pay insurance and are responsible for taxes -- so everyone is saying they hope the situation improves so they don't have to write down more foreclosures, but they aren't disappearing yet."

Roberts said it will likely take a couple of years -- and maybe even five or six -- for homebuilders to make a significant dent in inventories and for home sales to really begin recovering.

"Housing tends to be a long cycle, where it does really well for a long time and then you go down and stabilize for a long time as well," said Roberts. "For now sales will bounce up and down, but long term I don't think anyone is talking about a shortage of homes out there."

Tuesday, January 25, 2011

Rent vs. Own Ratio to Flip in 2011 ?

Many Americans are content to rent after witnessing the crumbling housing market in recent years. But with rents on the rise and home prices continuing to fall, a reversal is in sight.

It wasn't hard for many homeowners to bid adieu to 2010. It was the year where, in many metropolitan areas across the country, rents surged as home prices fell, leading a growing chorus of skeptics to question the so-called American Dream of homeownership.

It wasn't hard for many homeowners to bid adieu to 2010. It was the year where, in many metropolitan areas across the country, rents surged as home prices fell, leading a growing chorus of skeptics to question the so-called American Dream of homeownership.

Perhaps not surprisingly, it makes more financial sense to rent than buy today in many U.S. cities, according to the latest data from Moody's Analytics. After declining during the depths of the latest recession, prices for rentals nationwide increased modestly by about 3% in 2010, partly driven by a record number of homeowners looking for new digs after foreclosing on their homes. In Moody's latest list of rent ratios (which is the price of a typical home divided by the annual cost of renting that home) for 54 U.S. metropolitan areas, 39 fell into the 'better to rent' category -- roughly the same level it's been for the past year.

But that may finally be about to change. Moody's chief economist Mark Zandi expects the trend to reverse this year in many major cities. This would be a positive development, as a healthy housing market typically puts renting and owning at more equal footing.

"By mid 2011 and certainly by end of 2011, buying will be superior to renting in most parts of the country," Zandi says.

A few factors will be at play. For one, home prices are expected to fall further, with some economists expecting a 15% to 30% drop this year. This might be bad news for household finances and current homeowners fearing that their most prized asset stands to lose more in value. On the flip side, this makes homes more affordable and might finally spur more home sales, especially at a time when the rate of home construction has been the lowest since before the Second World War.

Just last week, the Case-Shiller index of property values reported a 0.8% fall in prices from October 2009 – the biggest year-over-year drop since December 2009. Eighteen of 20 cities showed a drop in prices in October. This was led by a 2.1% decrease in Atlanta, followed by a 1.8% drop in Chicago and Minneapolis. What's more, six markets, including Atlanta, Miami, Tampa and Portland, Ore., reached their lowest levels in October since prices started to retreat.

Indeed, the housing market continues to suffer from too much supply. Though rent prices are generally expected to continue rising modestly this year, the overhang will probably help keep prices from rising too much. "Expect more declines in home prices and more rent stability," Zandi says.

Still, the comparative costs between renting and buying will largely depend on individual market conditions. For instance, cities in Florida and Arizona, which continue to experience high foreclosure rates, falling home prices and widespread unemployment, will be areas where homeownership will likely be more affordable than renting, says Daisy Kong at Trulia, a San Francisco-based real estate data provider. Meanwhile, renting will probably continue to make more financial sense in national and regional job centers such as New York, Omaha and Seattle, she says.

And while it could become more attractive to buy than rent this year, it's anyone's guess how long it could take before a flurry of home sales transpires. Household finances have improved only modestly and are still quite a mess. Also, lending standards for new mortgages have tightened considerably and many economists have said a housing rebound will likely fall mercy to the unemployment rate, which is expected to improve some but still hover over 9%.

Will the American Dream return to your town?

Chicago, IL 15.09

Boston, MA 17.71

Hartford, CT 18.52

Long Island, NY 21.09

New York, NY 15.43

North - Central New Jersey 24.69

Bridgeport, CT 18.49

Manhattan, NY 28.34

Source: Moody's Analytics, price-rent ratio for third quarter of 2010. As a general rule of thumb, you should often buy when the ratio is below 15 and rent when it's above 20. If it's between 15 and 20, lean toward renting.

It wasn't hard for many homeowners to bid adieu to 2010. It was the year where, in many metropolitan areas across the country, rents surged as home prices fell, leading a growing chorus of skeptics to question the so-called American Dream of homeownership.

It wasn't hard for many homeowners to bid adieu to 2010. It was the year where, in many metropolitan areas across the country, rents surged as home prices fell, leading a growing chorus of skeptics to question the so-called American Dream of homeownership.Perhaps not surprisingly, it makes more financial sense to rent than buy today in many U.S. cities, according to the latest data from Moody's Analytics. After declining during the depths of the latest recession, prices for rentals nationwide increased modestly by about 3% in 2010, partly driven by a record number of homeowners looking for new digs after foreclosing on their homes. In Moody's latest list of rent ratios (which is the price of a typical home divided by the annual cost of renting that home) for 54 U.S. metropolitan areas, 39 fell into the 'better to rent' category -- roughly the same level it's been for the past year.

But that may finally be about to change. Moody's chief economist Mark Zandi expects the trend to reverse this year in many major cities. This would be a positive development, as a healthy housing market typically puts renting and owning at more equal footing.

"By mid 2011 and certainly by end of 2011, buying will be superior to renting in most parts of the country," Zandi says.

A few factors will be at play. For one, home prices are expected to fall further, with some economists expecting a 15% to 30% drop this year. This might be bad news for household finances and current homeowners fearing that their most prized asset stands to lose more in value. On the flip side, this makes homes more affordable and might finally spur more home sales, especially at a time when the rate of home construction has been the lowest since before the Second World War.

Just last week, the Case-Shiller index of property values reported a 0.8% fall in prices from October 2009 – the biggest year-over-year drop since December 2009. Eighteen of 20 cities showed a drop in prices in October. This was led by a 2.1% decrease in Atlanta, followed by a 1.8% drop in Chicago and Minneapolis. What's more, six markets, including Atlanta, Miami, Tampa and Portland, Ore., reached their lowest levels in October since prices started to retreat.

Indeed, the housing market continues to suffer from too much supply. Though rent prices are generally expected to continue rising modestly this year, the overhang will probably help keep prices from rising too much. "Expect more declines in home prices and more rent stability," Zandi says.

Still, the comparative costs between renting and buying will largely depend on individual market conditions. For instance, cities in Florida and Arizona, which continue to experience high foreclosure rates, falling home prices and widespread unemployment, will be areas where homeownership will likely be more affordable than renting, says Daisy Kong at Trulia, a San Francisco-based real estate data provider. Meanwhile, renting will probably continue to make more financial sense in national and regional job centers such as New York, Omaha and Seattle, she says.

And while it could become more attractive to buy than rent this year, it's anyone's guess how long it could take before a flurry of home sales transpires. Household finances have improved only modestly and are still quite a mess. Also, lending standards for new mortgages have tightened considerably and many economists have said a housing rebound will likely fall mercy to the unemployment rate, which is expected to improve some but still hover over 9%.

Will the American Dream return to your town?

Chicago, IL 15.09

Boston, MA 17.71

Hartford, CT 18.52

Long Island, NY 21.09

New York, NY 15.43

North - Central New Jersey 24.69

Bridgeport, CT 18.49

Manhattan, NY 28.34

Source: Moody's Analytics, price-rent ratio for third quarter of 2010. As a general rule of thumb, you should often buy when the ratio is below 15 and rent when it's above 20. If it's between 15 and 20, lean toward renting.

Existing Home Sales Jump 12%

Sales of existing homes jumped in December, marking the fifth month of gains in the past six months, based on an industry report released Thursday.

Previously-owned home sales climbed 12.3% in December to an annual rate of 5.28 million, from 4.70 million in November, according to the National Association of Realtors.

That puts sales at the highest level since the homebuyer tax credit expired in June, said Stuart Hoffman, chief economist at PNC Financial Services Group.

The December rate came in much higher than expected. A consensus of experts surveyed by Briefing.com had forecast an annualized sales rate of 4.8 million. However, sales were down 2.9% from 12 months earlier and fell 4.7% in 2010.

"December was a nice finish to the year, but looking at the bigger picture -- home sales and prices have been scraping along the bottom for the last three years," Hoffman said. "So, while we're not digging a deeper hole -- the housing market is still quite weak, and there are still more homes available on the market than there are likely to be buyers."

The median price of all existing homes sold in December was $168,800, down 1% from a year ago.

Previously-owned home sales climbed 12.3% in December to an annual rate of 5.28 million, from 4.70 million in November, according to the National Association of Realtors.

That puts sales at the highest level since the homebuyer tax credit expired in June, said Stuart Hoffman, chief economist at PNC Financial Services Group.

The December rate came in much higher than expected. A consensus of experts surveyed by Briefing.com had forecast an annualized sales rate of 4.8 million. However, sales were down 2.9% from 12 months earlier and fell 4.7% in 2010.

"December was a nice finish to the year, but looking at the bigger picture -- home sales and prices have been scraping along the bottom for the last three years," Hoffman said. "So, while we're not digging a deeper hole -- the housing market is still quite weak, and there are still more homes available on the market than there are likely to be buyers."

The median price of all existing homes sold in December was $168,800, down 1% from a year ago.

Subscribe to:

Posts (Atom)